Impact of Budget 2078-2079 on Business & Taxation

Finance Minister Bishnu Prasad Poudel presented the Budget of Nepal for fiscal year 2078-2079 on 15th of Jestha, 2078. Finance Minister through this annual budget attempts to mitigate the economic effects of COVID on economy, promising to support the businesses to get back on the run.

We have compiled all the facts from the Budget Speech and Financial Ordinance with respect to its impact on Business & Taxation.

Click the button below to download the Budget Summary of FY 2078-2079, Nepal or you can go through the whole article.

1. Objectives of Budget FY 2078-79 with respect to Taxes & Revenue

- Tax Discount and concessions to COVID affected industries.

- Protection of domestic industry and simplification of business

- Increase in scope of Tax and control over tax evasion.

- Progressive, Healthy transparent, and automated revenue process

- Infrastructural development and use of Information technology.

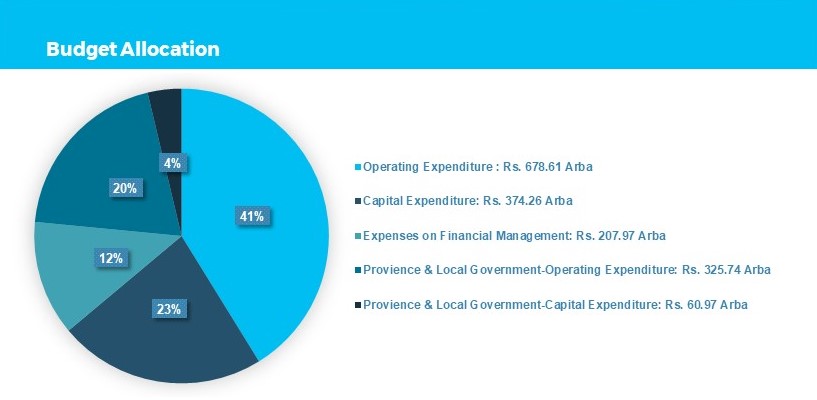

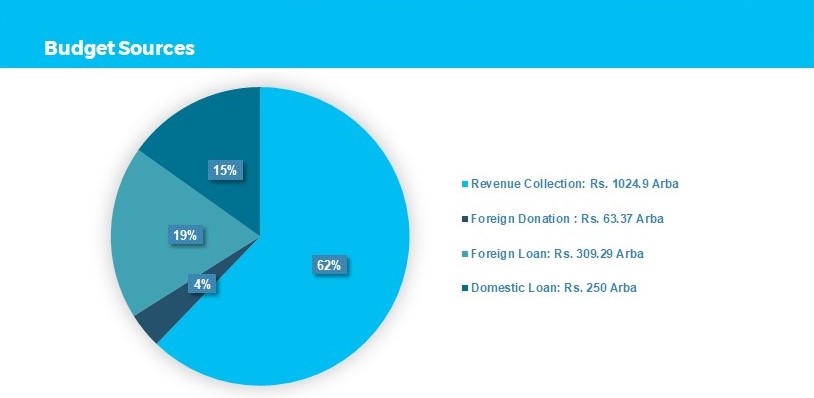

2. Budget Allocation & Sources

Budget Allocation

| Particulars | Amount ( In Arba) |

| Total Budget | 1,647.57 |

| Operating Expenditure | 678.61 |

| Capital Expenditure | 374.26 |

| Expenses on Financial Management | 207.97 |

| Province & Local Government | |

| Operating Expenditure | 325.74 |

| Capital Expenditure | 60.97 |

Budget Source

| Particulars | Amount ( In Arba) |

| Revenue Collection | 1024.90 |

| Foreign Donation | 63.37 |

| Foreign Loan | 309.29 |

| Domestic Loan | 250.00 |

3. Tax Reliefs for FY 2077-2078

- Income Less then 20 Lakhs u/s 4(4): 90% Tax Rebate

- Income more than 20 Lakhs and less than 50 Lakhs u/s 4(4a): 75% Tax Rebate

- Income more than 50 lakhs and less than 1 Crore: 50% Tax Rebate

4. Tax Relief for COVID Affected Businesses

- Hotel, Travel, Transportation, Airlines, Cinema & Film making

- Tax Rate for FY 2077-2078: 1% of Taxable Profit

- Carry forward of loss: 10 years for the losses related to FY 2076-2077 and FY 2077-2078

- Hotel and Tourism, Public transportation, Cinema, Airlines, Handicrafts, Advertising, Tailoring, Beauty Parlors, Health Clubs:

- Registration and renewal fees for FY 2078-2079 waived off

5. Promotion & Encouragement of Start-Ups

- Turnover up to 1 crore: Tax Exempt for 5 years from the year of operation

- Contribution made by any person to startup as seed investment to the extent of Rs 1 Lakh for up to 5 startups: Deductible form Income

- Loan for Startups: up to 25 Lakhs at the rate of 1% against the collateral of project

6. Improvements on Value Added Tax (VAT)

- Diesel and LPG used in Vatable business: Input VAT Credit available

- VAT Exempt Businesses:

- Freight and transportation Services

- Cargo Services

- E-Library Services

- Trekking and Tour Packages

7. Exemptions & Benefits on VAT, Excise Duty & Import Duty

- VAT, Import Duty and Excise Duty: Exempt (up to Poush Masanta 2078)

- Oxygen Gas

- Liquid Oxygen

- Oxygen Cylinder

- Oxygen Concentrator or

- Any survivor equipment or medicines

- Excise Duty: Exempt – Import Duty: Reduced

- Electrical Vehicle

- Refrigerator

- Grinder

- Rice Cooker

- Fan

- Other electronic appliances

- Import Duty: Exempt

- Equipment or spare parts used in : Tea, Jute, Cinema, Pashmina, Hatchery, Agricultural or Nursery Industries

- Import Duty: Reduced

- Import of Container by Shipping Company registered in Nepal

- Baby milk products: Import Duty reduced by 50%

- Induction Cooktops: Import Duty reduced to 1%

- Liquors, Cigarette, tobacco products and Carbonated Soft Drinks: Increase in Excise Duty

8. Broadening of Scope of Income Tax Act, 2058

- Presumptive tax u/s 4(4): D-01 Tax return

- Turnover: Up to 30 Lakhs (Previously 20 Lakhs)

- Income: Up to 3 Lakhs (Previously 2 Lakhs)

- Tax based on turnover u/s 4(4A): D-02 Tax Return

- Turnover: Above 30 Lakhs to 1 Crore (Previously 20 Lakhs to 50 Lakhs)

- Income: Up to 10 Lakhs

- Tax Rates:

- For Turnover 30 Lakhs to 50 Lakhs: 1%

- For Turnover above 50 Lakhs to 1 Crore: 0.8%

- Service Sector: 2%

- Tax Rates:

- Important: Compulsory for everyone even if registered under VAT, except in the case of the service sector with respect to D-02

- TDS @5%

- Payment to foreign colleges or university as registration fees, exam fees or tuition fees

- Payment made to Life Insurance company by Domestic BFIs as interest on deposit

- Sale of listed shares by Resident Individual Person

- Short Term Capital Gain (held less than 365 days) :7.5%

- Long Term Capital Gain (held more than 365 days) :5%

- Any person providing offshore online services and receive payment in foreign currency: TDS @1% (By any agency making such transfer to such person)

9. Exemptions & Rebates under Income Tax Act, 2058

- Income Tax: Exempt

- Income form Mutual Funds

- Surplus by Non profitable organization in partnership with Nepal government or any government organization engaged in providing educational services

- No TDS

- Payment of Interest on loan by Banks to International Financial Institution

- Payment of interest on loans among co-operative banks or organization

- Income from Agricultural Business: 50% Concession in tax rate

- Income form domestic production and sales of raw material and auxiliary raw materials to specialized Industry: 20% Rebate on income tax

- Income form export by specialized industries: Tax Rate 10% (Earlier 15%)

- Additional 25% exemption on calculation of taxable income from pension income.

- 50% Tax Rebate for first 3 years, 25% for next 2 years from the year of production

- Industries using recyclable Hazardous waste as raw materials

- Any Industry established or relocated inside an Industrial area

- 100% Tax Exempt for 3 years and 50% for next 2 years from the year of operation

- Any industry currently operating in Kathmandu Valley relocated outside Kathmandu

10. Allowable Deductions under Income Tax Act, 2058

- Deduction allowed in FY 2077-2078

- Contribution made in FY 2077-2078, to government fund established for the control and treatment of COVID-19 infections

- Amount is paid in FY 2077-2078 as CSR for establishment of specialized hospital as specified by MoHP or expenses on equipment or medical tools used for treatment of COVID-19

- Payment made by transport agencies to any individual vehicle owner even without invoice, if TDS is deducted as per the Income Tax Act. (Only for FY 2076-2077)

- Insurance premium paid for insurance of private house upto Rs.5000 allowed as deduction for resident individual.

11. Improvements in Tax Administration & Procedures

- Electronic Tax Clearance: For all the taxpayers with no outstanding tax and have settled all the self assessed taxes.

- Eventually, all the VAT Registered entities will be brought under the scope of electronic billing.

- Verification of Sales & Purchase Register from Tax officer: Not Required

- Renewal of EXIM Code: For a period of 5 years at once

- Bank Guarantee can be used instead of depositing tax amount in case of technical review at IRD or Appeal at the Tribunal

12. Benefits & Reliefs for Social Security Funds

- Transfer of amount from approved retirement fund to SSF by any person registered or intended to register under SSF by Chaitra Masanta 2078: No TDS on such withdrawal of funds from Retirement fund.

- SSF Contribution for Jestha-78 and Ashad-78: Borne by government

13. Waiver under Income Tax Act, 2058

- If a company or firm, not filing annual returns and nonrenewal till FY 75-76, files annual returns and pay 10% of total fines & Penalties by Ashwin Masanta 2078 and balance 90% of fines and penalties will be waived off.

- If any case is pending against the tax assessment under Income Tax Act,2058, Value Added Tax Act, 2052 or Excise duty Act, 2058 up to Ashad Masanta 2077 with the Revenue tribunal or Court, except the case of forged or fake invoices, concerned assessee can pay the tax amount in full and 50% of the interest by Mangsir Masanta 2078 and rest of the Interest, fines and penalties will be waived off.

- Any outstanding tax related up to assessment up to the Financial year ending 2076 and interest thereon under Income Tax Act,2058, Value Added Tax Act, 2052 or Excise duty Act, 2058: if paid by Poush Masanta 2078, additional fines, penalties and any other charges will be waived off.

- Any assessment of tax under VAT Act or Income Tax Act upto 15 Jestha 2078 against not-for-profit Cooperative hospital and companies providing online based transportation services: Waive off all the outstanding amounts if applied for it till Poush Masanta 2078

- Trekking & Tour Agency: If any of the vatable services related to trekking and tours packages are being rendered as non vatable services, Self declaration of such transaction upto Jestha 14 2078 is done, and if VAT levied on such self declared services are paid by Poush Masanta 2078, additional interest, fines and penalties will be waived off

- Trekking & Tour Agency: Any tax assessment by the IRD with respect to Non vatable services and amount outstanding thereon, if paid by Poush Masanta 2078, additional interest, fines and penalties will be waived off

Click the button below to download the Budget Summary of FY 2078-2079, Nepal.

Next Post

Next Post

Really impressed with the professionalisn, expertise and quality of work of the Think Professionals team. They understand the Nepal Govt Laws and Policies well enough and execute work with simplicity and at the best interest and understanding of the Company. Truly Recommmend and Best wishes to the team.

-Romit Bajracharya